Robust Regression Using Regular JMP 18 version powered by Python Integration

Enhance your regression analysis with the powerful combination of robust techniques and JMP 18, now featuring seamless integration with Python. Simple Case Study Here's a sample...

DaeYun_Kim

DaeYun_Kim

83 views

|

0 replies

Richard_Zink

Richard_Zink

SamGardner

SamGardner

KristenBradford

KristenBradford

Chris_Kirchberg

Chris_Kirchberg

cweisbart

cweisbart

Paul_Nelson

Paul_Nelson

Craige_Hales

Craige_Hales

anne_milley

anne_milley

Di_Michelson

Di_Michelson

JohnPonte

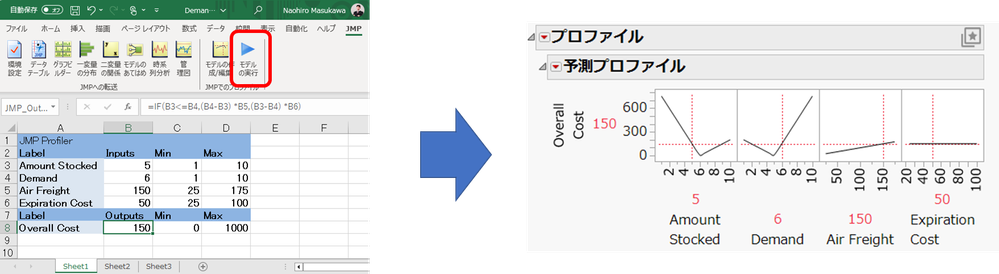

JohnPonte Masukawa_Nao

Masukawa_Nao

Jed_Campbell

Jed_Campbell LauraCS

LauraCS MarilynWheatley

MarilynWheatley chris_gotwalt1

chris_gotwalt1

gail_massari

gail_massari